AI SHORT-TERM RENTAL SOFTWARE

The future of vacation rental management, built on AI.Vacation rental management, built on AI.

Optimize every aspect of property management, from channel distribution to revenue and guest experience. You set the rules, Guesty’s AI handles the rest.

Optimized property management, channel distribution, and revenue. You set the rules, our AI handles the rest.

What are you most interested in?

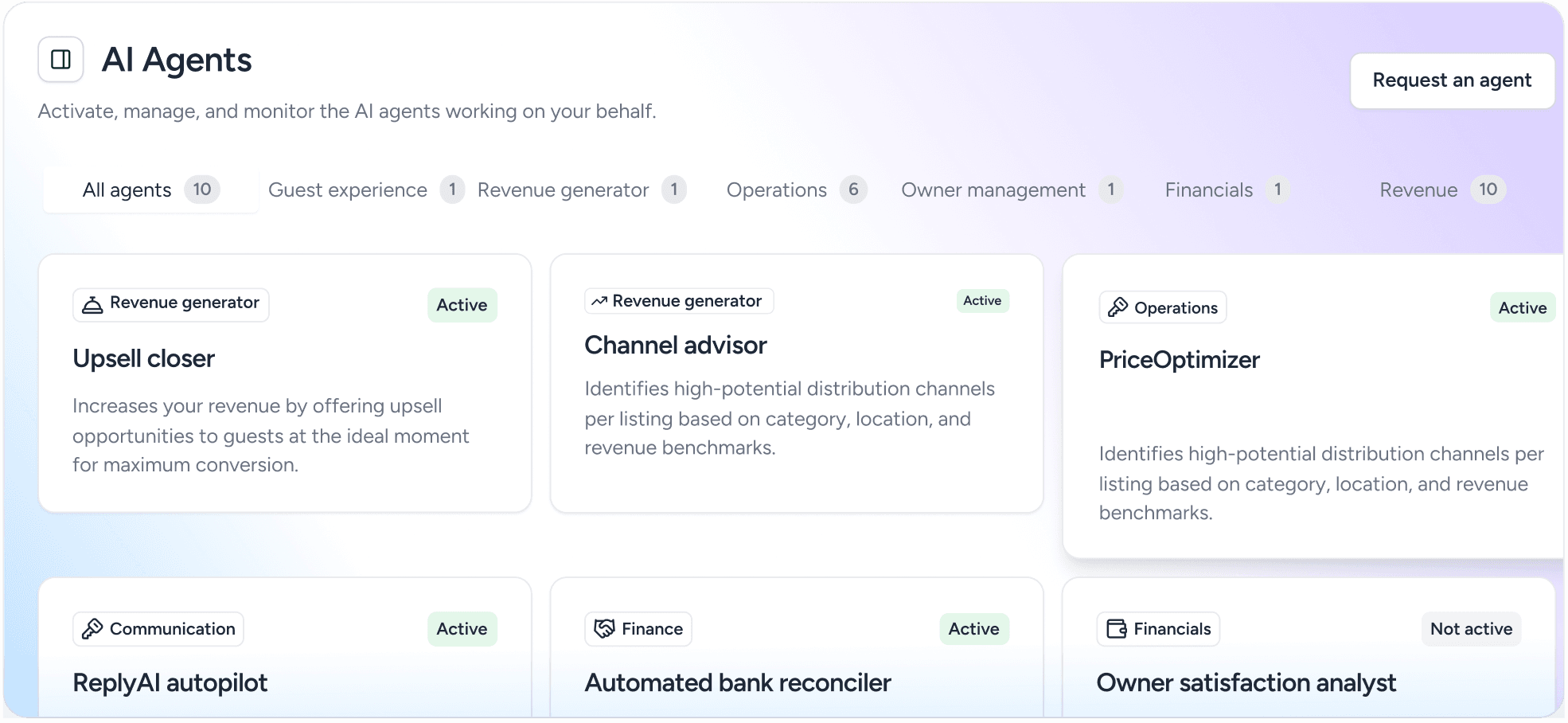

All Guesty AI agents

AI-powered guest comms

Channel management

Multi-calendar

AI revenue management

AI-optimized website

How it works

Manage your vacation rental properties and channels, from one

AI-powered platform

Eliminate double bookings

Sync your properties in real-time on Airbnb, Booking.com, Vrbo, and 60+ channels, instantly optimizing for top rankings and AI search results

Orchestrate your operations

Delegate your most demanding tasks to AI agents that act, decide, and execute on your behalf, all coordinated from one intuitive dashboard.

Grow your revenue

Drive revenue through dynamic pricing, AI-powered analytics, and elevated guest experiences that set you apart from the competition.

From solo to scale

Your vacation rental business has no limits.

Neither do we.

Smart tools for solo hosts

Guesty Lite gives solo hosts running 1-3 listings everything they need to run a vacation rental: AI-powered guest messaging, automated workflows, and real-time channel sync with Airbnb, Vrbo & Booking.com.Discover Guesty Lite™

Agentic AI for professional property managers

Guesty’s AI agents multiply your team, helping vacation rental companies evolve from just a few properties into regional leaders that manage hundreds of listings and drive millions in revenue.Discover Guesty Pro™

Custom intelligence for enterprise operators

Property management enterprises rely on Guesty's customized solutions to manage thousands of listings, optimize revenue, and deliver exceptional guest experiences globally. Use our team of AI agents, or build your own with our open API.Discover Guesty Enterprise™

Everything under one roof

Every feature you need to manage your short-term rental business.

Distribute across 60+ OTAs

with smart, channel-specific

dynamic pricing strategies

- Connect to Airbnb, Vrbo, Booking.com & 60+ booking channels

- Tailor rate strategies for each channel

- Sync availability and pricing in real-time

- Build branded direct booking websites for your short term rental brand

- Connect to Airbnb, Vrbo, Booking.com & 60+ booking channels

- Tailor rate strategies for each channel

- Sync availability and pricing in real-time

- Build branded direct booking websites for your short term rental brand

- A single unified inbox for all guest communication

- A multi calendar for every reservation

- Metrics to track and benchmark KPIs

- Customizable business reporting

- Automated end-to-end guest journey

- AI generated personalized guest replies

- AI-driven website content creation

- Mobile app for on-the-go management

- User-friendly guest portal

- CRM turns data into guest satisfaction

- Automated review collection

- AI summaries to improve reviews

- Machine learning driven dynamic pricing

- Pricing rules for every scenario

- Integrated, secure payment solutions

- Compliant vacation rental trust accounting

- Comprehensive liability protection

- Damage protection coverage

- AI-powered fraud prevention tools

- Thorough guest verification

Hundreds of AI agents,

one mission: yours

From dynamic pricing to guest communication, Guesty AI acts across every part of your vacation rental workflow to drive better results.

Data intelligence

Get instant, plain-language answers about your revenue, occupancy, and portfolio performance, straight from your live Guesty data.

Bank Reconciliation

Streamline your reconciliation process with AI that automatically reviews and matches your transactions, eliminating hours of manual financial admin.

Revenue optimization

Make smarter pricing decisions with machine learning algorithms that monitor your market in real-time and automatically adjust your rates for maximum revenue.

Reviews management

Build trust with AI-powered review analysis that surfaces actionable improvements from guest feedback, and generates thoughtful, on-brand responses automatically.

Revenue protection

Safeguard your business with AI that screens every booking, identifies high-risk transactions, and stops fraudulent payments before they reach you.

Listings descriptions

Get to market faster with AI-generated listing descriptions crafted to perform across every channel and your direct booking website.

Website builder

Drive more direct bookings with AI-generated site content, meta tags, and SEO structures designed to boost your search visibility and conversion rate.

Guest messaging

Save time on manual communication with an AI agent that reads incoming messages, detects sentiment, and crafts personalized, on-brand replies in any language.

Real voices, real results

Hear from short-term rental operators who are growing their business with Guesty

Fueled by exploration and innovation, Guesty's comprehensive software suite delivers the tools you need to scale your portfolio and stay ahead

portfolio increase in 2 years

“There are a lot of options when it comes to property management software, but having one that grows with the industry has been super helpful for us”

hours on average saved per month

revenue growth in 2 years

properties added in 5 years

increase in daily rates

hours on average saved per month

revenue growth in 2 years

properties added in 5 years

increase in daily rates

THE GUESTY PROMISE

Customer support you can always count on

Onboarding

Our onboarding team is dedicated to your success. With a range of onboarding programs, from 1-on-1 software adoption sessions to in-depth project planning and listings migration, your success at Guesty is our priority.

Touch points

Book a demo24/7 chat support

Get the help you need when you need it. Guesty's support team is available 24/7 to help with urgent issues or answer any questions that might arise.

Touch points

Book a demoKnowledge

We're here to help you grow with Guesty, whether its through our user-ready Guesty Academy, our dedicated customer success managers, or our robust knowledge center, we help you make the most of your Guesty experience.

Touch points

Book a demoTouch points

Book a demoConnect with 200+

top industry solutions

Guesty's Marketplace helps you build a stronger tech stack and manage everything from one place with integrations to 200+ booking channels and third-party solutions through its open API.

Built by hosts, trusted

by industry leaders

worldwide

listings managed across

our platform

uptime backed by

24/7 support

feature releases to

keep you ahead

R&D experts driving

continuous innovation

Industry Recognized Excellence

See why property

managers around the

globe rely on Guesty

We've had zero double bookings since using Guesty and I think that ties directly to the Multi-Calendar.

Roami

Double bookings in our combined units led to a lot of wasted time for our guest experience agents. Having the automated calendar rules prevents all of that.

Zen Vacation Rentals

Guesty has been pivotal in a lot of our growth. A lot of it boils down to the guest communication, which for us has been a life saver.

Old Town Rental

There are a lot of options when it comes to property management software, but having one that grows with the industry has been super helpful for us.

Daniel & Jacob's Apartments

Guesty makes it easy to scale up. It feels like it’s built for that.

Great Dwellings

Guesty has been the reason we've been able to grow. Besides my amazing team, it allows you to be bigger than you are.

Angel Host

Because Guesty is a very robust platform, we were not afraid to move from five properties to 500 in three years.

It's just at your fingertips — you can see which platforms properties are booked on and go from there. Less manual handling is a huge factor in reducing staff stress.

We've had zero double bookings since using Guesty and I think that ties directly to the Multi-Calendar.

Roami

Double bookings in our combined units led to a lot of wasted time for our guest experience agents. Having the automated calendar rules prevents all of that.

Zen Vacation Rentals

Guesty has been pivotal in a lot of our growth. A lot of it boils down to the guest communication, which for us has been a life saver.

Old Town Rental

There are a lot of options when it comes to property management software, but having one that grows with the industry has been super helpful for us.

Daniel & Jacob's Apartments

Guesty makes it easy to scale up. It feels like it’s built for that.

Great Dwellings

Guesty has been the reason we've been able to grow. Besides my amazing team, it allows you to be bigger than you are.

Angel Host

Because Guesty is a very robust platform, we were not afraid to move from five properties to 500 in three years.

It's just at your fingertips — you can see which platforms properties are booked on and go from there. Less manual handling is a huge factor in reducing staff stress.

Frequently asked questions

Here is what some of our

customers needed to know

before signing up

What is Guesty?

Guesty is an all-in-one AI powered vacation rental software designed for short-term rental hosts and property managers. Whether you're managing a single vacation rental or a large portfolio, Guesty streamlines your operations by automating reservations, guest communication, channel management, and payments in one place. With AI-powered tools built in, you can automate routine tasks, optimize pricing, and deliver exceptional guest experiences while saving time and growing your business.

Is Guesty a good fit for hosts with 1–3 properties?

Yes. Guesty Lite is built exactly for hosts and property managers with 1-3 properties. You get real-time sync across Airbnb, Vrbo, and Booking.com, a unified inbox for all guest messages, automated messaging, task management for cleaners, and a direct booking website — starting at $9/month. The key difference from tools built only for small hosts: when you add your fourth property, you upgrade your plan, not your platform. Your automations, integrations, and guest data all carry forward.

How do I get started with Guesty, and is there an onboarding process?

Getting started with Guesty is straightforward. After signing up, you'll go through a guided onboarding process that helps you connect your properties, link your booking channels, set up automated messaging, and configure your account settings. Our team provides personalized support to ensure you're set up correctly from day one, and we offer training resources to help you master the platform quickly.

What kind of customer support does Guesty offer?

Guesty provides comprehensive support to all customers through multiple channels including 24/7 live chat, email, and phone support. You'll also have access to our extensive help center with articles, video tutorials, and guides. Our support team is knowledgeable about the platform and the short-term rental industry, so we can help you troubleshoot technical issues and answer operational questions to keep your business running smoothly.

What booking channels does Guesty connect to?

Guesty's Channel Manager connects to 60+ booking channels, including Airbnb, Vrbo, Booking.com, Expedia, Google Travel, Hopper, and Homes & Villas by Marriott Bonvoy. All connections are direct API integrations — not iCal feeds — meaning availability and pricing update across every channel in real time the moment a booking comes in.

How much does Guesty cost?

Guesty pricing starts at $9 per month and scales with your business. . Visit our pricing page to see which plan fits your business.